Escalating trade frictions between the United States and Canada have entered a new phase after the Trump administration unveiled a steep 50% tariff on a targeted set of Canadian imports, a move analysts frame as both a high-stakes negotiating tactic and a strategic shift in legal authority that carries significant risks for bilateral economic relations. Announced publicly by U.S. President Donald Trump on Monday, the new tariffs apply to a range of Canadian goods including wine, hockey sticks, and cement, covering nearly $20 billion in annual cross-border shipments, according to trade experts. The White House has justified the measure as a response to what it calls discriminatory trade practices from Canada, encompassing Canadian restrictions on U.S. alcohol distribution, the country’s longstanding dairy supply management system, and existing automobile import quotas. Canadian Prime Minister Mark Carney swiftly issued a sharp condemnation of the new tariffs, characterizing the action as the latest in a string of unilateral trade measures imposed by Washington that directly violate the terms of the Canada-United States-Mexico Agreement (CUSMA), the regional trade pact that has governed North American commerce for years. Despite the condemnation, Carney stressed that Canada remains open to intensive talks to resolve outstanding trade disputes, noting that a negotiated settlement would deliver mutual benefits for citizens of both countries. The announcement has also sparked pressure from Canadian subnational leaders: Ontario Premier Doug Ford, whose province is among Canada’s largest exporters to the U.S., called on the federal government in Ottawa to hit back with reciprocal measures. In a social media post, Ford wrote, “I’ll never stop fighting to protect Ontario. If these tariffs proceed, Canada should respond tariff for tariff, dollar for dollar.” Trade analysts and academic experts say the latest tariff announcement marks two key shifts in the Trump administration’s approach to trade pressure on Canada. First, it leverages a little-used legal authority from the 1930 U.S. Trade Act, known as Section 338 – a departure from the 1962 and 1974 trade acts that the administration relied on for earlier tariffs, which have run into legal challenges. Dave Townsend, a partner in Dorsey & Whitney’s International Trade Group, explained that this new legal framework allows the Trump administration to impose duties even on goods that are normally granted duty-free access under the terms of CUSMA. The tariffs are set to go into effect 30 days from the announcement date, and Townsend noted their timing is tightly tied to the ongoing, stalled negotiations between Washington and Ottawa. “Canada has thus far not agreed to a new framework trade agreement with the United States, and the White House explicitly noted that only Canada and China have failed to reach such pacts, with both countries having retaliated against earlier U.S. tariffs,” Townsend explained. “Thus, the higher tariffs for goods from Canada appear to be aimed at encouraging an agreement between Canada and the United States, or in retaliation for the failure to reach such agreement, or both.” The new measure raises the risk of further deterioration in already strained bilateral relations, Townsend added. “The question now is whether the two sides can reach such an agreement or whether a cycle of escalation and retaliation takes hold between the two countries.” Ronald Stagg, a history professor at Toronto Metropolitan University, pointed out that turning to the 1930 Trade Act carries historical echoes of economic catastrophe: the act’s original use in the 1930s triggered widespread retaliation from trading partners that deepened the global Great Depression. Stagg also noted that the announcement caught many Canadian policymakers and observers off guard, as public attention had been focused on Trump’s recent threats to penalize Canada over wildfire smoke that drifted across the border, where he accused Canada of failing to manage its forest resources properly. Just days before the tariff announcement, Trump was publicly attacking Canada over the wildfire issue, making the trade move an unexpected shift in focus. Stagg added that the tariff move aligns with a long-observed pattern in Trump’s approach to international negotiations, where he seeks to extract financial or political concessions from counterparties. He pointed to the years-long hold-up of the Gordie Howe International Bridge, a critical new cross-border infrastructure project connecting Detroit, Michigan, and Windsor, Ontario, as a clear example. “His refusal to allow the Gordie Howe Bridge to open until the United States, or possibly the owner of the competing Ambassador Bridge, a significant donor to the Republican Party, received additional compensation, is a good example,” Stagg said. “This demand came despite Canada having paid for the construction, in cooperation with Michigan. The issue for Trump is, on what grounds can he demand money for the United States, or his financial supporters, or his family in each situation.” With the new tariffs in place, the ball is now in Canada’s court to decide how to respond, Stagg noted. “The question now is, will Canada retaliate, or will the Canadian government complain, but try not to ‘poke the bear’?”

分类: business

-

Asian shares mostly gain and South Korea and Japan recover some losses from AI stock sell-offs

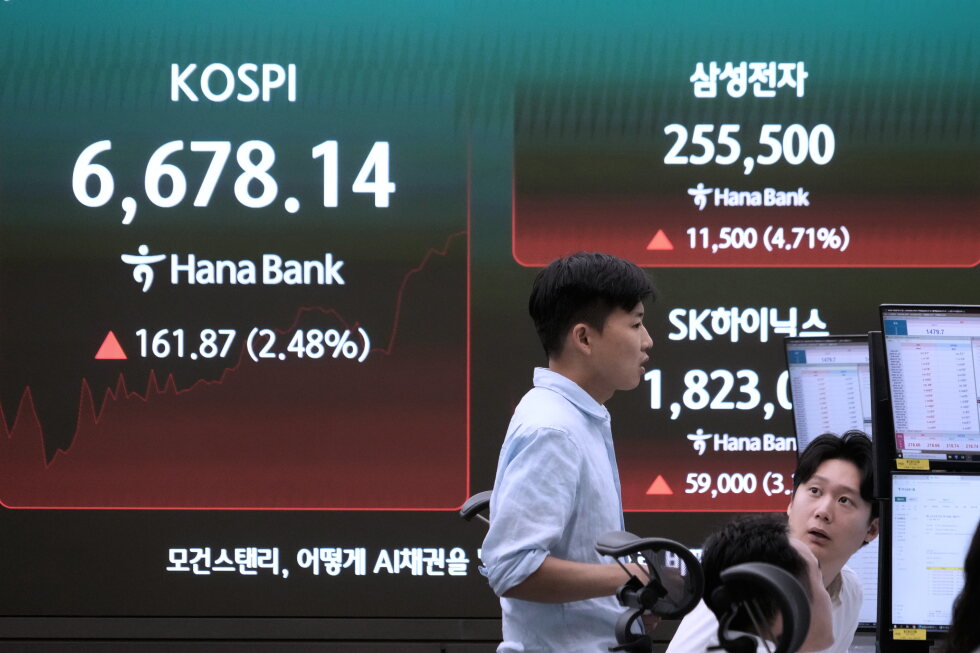

After a sharp sell-off of artificial intelligence-linked equities that dragged down major regional benchmarks in recent weeks, most Asian stock markets staged a notable rebound during Tuesday’s trading session, while U.S. futures ticked modestly upward and global crude prices edged lower amid ongoing Middle East geopolitical instability.

South Korea’s benchmark Kospi index, which has a heavy concentration of AI and semiconductor manufacturing stocks, led the recovery with a 4.7% jump to close at 6,821.41. This strong gain came one day after the index dropped 4.5%, and reverses part of the broader 20% correction the Kospi has seen over the past month. Despite the recent pullback, the index has still delivered a total gain of more than 50% since the start of the year. The sell-off was driven by investor profit-taking, fueled by growing concerns that AI-focused investments may have formed a speculative bubble. Leading the upward move on Tuesday, Samsung Electronics surged 7.4%, while major memory chip producer SK Hynix climbed 6.4%.

In Japan, the Nikkei 225 gained 2.8% to reach 65,926.41, recovering a portion of last week’s losses after Japanese markets were closed for a public holiday on Monday. Chip-related stocks also led gains in Tokyo: memory manufacturer Kioxia Holdings jumped 15.9%, chip testing equipment maker Advantest rose 6.9%, OpenAI investor SoftBank Group added 6.1%, and chip equipment producer Tokyo Electron gained 1.3%. Further along the Asian tech supply chain, Taiwan’s Taiex index, which has also outperformed this year amid the global AI boom, climbed 3.6%, with leading advanced AI chip manufacturer TSMC advancing 2.8%.

In other East Asian markets, Hong Kong’s Hang Seng Index edged less than 0.1% higher to 25,150.75, while mainland China’s Shanghai Composite Index added 0.6% to 3,819.66. Australia’s S&P/ASX 200 notched a modest 0.1% gain to 8,798.00, while India’s Sensex ticked 0.1% lower in Tuesday trading.

Global oil prices slipped lower in early Tuesday trading after rising in the prior session. International benchmark Brent crude fell 0.7% to $88.63 per barrel, dipping below the $90 threshold, while U.S. benchmark crude lost 0.3% to trade at $82.24 per barrel. Even with the drop, both benchmarks remain far above levels seen before the outbreak of regional conflict in late February, when Brent traded around $72 per barrel.

Oil price movements come amid escalating and sustained geopolitical tension across the Middle East. Early Tuesday, Iran launched an attack on another commercial tanker transiting the Strait of Hormuz, the critical global chokepoint that carries roughly a fifth of the world’s daily oil and gas supplies. The U.S. has launched its 10th consecutive night of airstrikes targeting Iranian assets, and Iran has retaliated against U.S. allies across the region. In a tentative step toward diplomacy, Iran’s interior minister traveled to Pakistan, a key regional mediator, for talks aimed at de-escalation, though it remains unclear whether any negotiated breakthrough can be reached.

“In the current environment, there is some hope that tensions between the U.S. and Iran can cool,” ING commodities strategists Warren Patterson and Ewa Manthey noted in a Tuesday market commentary. They added, “This will not be a straightforward process, however, as deep divisions still remain between the two sides.” The analysts also pointed to added supply risk from another ongoing conflict: a naval blockade imposed by Yemen’s Iran-aligned Houthi movement on Saudi shipping has raised the threat of disruptions to global oil exports.

On Wall Street, major U.S. benchmarks closed slightly lower in Monday’s session: the S&P 500 slipped 0.2% to 7,443.28, the Dow Jones Industrial Average fell 0.6% to 51,839.26, and the tech-heavy Nasdaq Composite dipped less than 0.1% to 25,508.07. Even with the overall minor dip for the benchmark indexes, many leading U.S. AI and chip stocks posted gains: Nvidia rose 0.2%, Micron Technology climbed 1.9%, Broadcom gained 2%, and Advanced Micro Devices (AMD) added 1.6% following the announcement of an expanded AI partnership with Microsoft. In currency markets Tuesday, the U.S. dollar edged slightly lower to 162.48 Japanese yen, down from 162.50 yen on Monday, while the euro held steady at $1.1414.

This report was contributed to by AP Business Writers Stan Choe and Matt Ott.

-

KPMG names new leader as firm battles to rebuild trust after scandal

One of Australia’s largest professional services firms, KPMG Australia, has named John Sams as its permanent chief executive with immediate effect, marking a key step in the firm’s effort to recover from a damaging whistleblower scandal that forced out its entire previous top leadership. Sams, a 30-year veteran of the firm, draws his experience from KPMG’s tax, corporate finance and infrastructure advisory divisions — the part of the business that has not been implicated in the misconduct that shook the firm over the past three months.

The scandal that toppled the previous leadership broke when a whistleblower exposed that KPMG audit partners had circulated unredacted, sensitive internal client data from competing firms to win new auditing contracts. When the employee raised formal concerns about the unethical practice, senior executives not only dismissed the allegations but also allegedly orchestrated efforts to push the whistleblower out of the company.

By the end of June, the fallout had forced sweeping leadership changes: both former chairman Martin Sheppard and chief executive Andrew Yates resigned, alongside two senior audit partners, Paul Rogers and Eileen Hoggett. Interim CEO Stan Stavros stepped in to oversee immediate reforms, acknowledging publicly that the firm had failed to meet the professional and ethical standards expected by the public, regulators, and clients. At the time, Stavros outlined a multi-pronged reform plan, including overhauling leadership, strengthening independent governance, launching independent external reviews of firm culture and practices, improving whistleblower protection mechanisms, tightening internal controls, and embedding clearer accountability across all levels of the organization. He emphasized that trust could only be restored through consistent, tangible action rather than empty promises.

In the announcement of Sams’ permanent appointment, independent board chair Michael Ebeid said the board had full confidence that Sams possessed the agility, courage, and integrity required to lead the firm through its rebuilding phase. Ebeid laid out a clear mandate from the board for the new CEO: strengthen firm leadership and internal culture, repair damaged confidence among KPMG staff, clients, industry regulators, and Australian government and parliamentary bodies, and refocus the firm on delivering value to all its stakeholders. Sams has the full backing of the board to fully implement the June action plan addressing governance and integrity failures, with the goal of building a more transparent and accountable firm, Ebeid added.

Accepting the role, Sams acknowledged he does not underestimate the scope of the challenges ahead. “The firm fell short of the standards rightly expected of us, and the accountability for these failures will continue to be implemented,” he said. “We have serious work to do on our culture, our leadership and our governance and it will take resolve and endurance.” Sams committed to making the difficult but necessary decisions to put the firm back on an ethical and sustainable path.

-

More jobs to be cut at Nine in shift to ‘digital-first future’

Australian media giant Nine Publishing has confirmed another wave of staff redundancies, as the company accelerates its strategic transition away from legacy print operations toward a digital-first media model. The new cuts come as part of a broader organizational and operational overhaul that has been unfolding across the company’s news and publishing division throughout 2024.

In an internal email sent to all publishing staff on Tuesday morning, Nine Publishing executive Tory Maguire notified employees of an urgent town hall meeting to outline the details of the upcoming structural changes. Maguire framed the restructuring as a necessary adaptation to a rapidly shifting global media ecosystem, arguing that organizational change was critical to protecting the company’s core commitment to high-quality journalism.

“ The best way to protect our quality journalism is to ensure our organisation adapts to a changing media landscape, that we’re growing commercially and investing in new areas which connect with new audiences. In particular we need to keep shifting towards the digital-first future,” Maguire wrote in the staff memo. “Therefore, we are constantly reviewing our business to ensure it is fit for purpose in our changing environment. As a result we are going to be making some changes to our structure and how we operate.”

This latest round of redundancies builds on a previous round of cuts announced back in April, when Nine’s parent company carried out the first sweep of layoffs that eliminated 20 roles across the firm’s news and current affairs division. At that time, leadership framed the restructuring as tied to the rollout of the company’s flagship Future News project, an initiative designed to upgrade the network’s technology infrastructure, staff training, and production equipment while streamlining workflows and pushing for more multiskilled roles across the newsroom.

Nine’s executive director of news and current affairs Fiona Dear described the Future News project in April as the largest single investment in the company’s news and current affairs division in decades. She noted that new digital tools, integrated systems, and updated production workflows were set to completely transform how the organization creates and distributes news content.

“We’ve said from the beginning that this will touch all roles in some way, shape or form,” Dear said in April. “This isn’t about doing the same work with fewer people to save money; it’s about acknowledging that the work itself is changing across our industry and we must adapt to survive and thrive.”

As of Tuesday, company leadership has not released the exact number of roles set to be eliminated in this latest restructuring round, with additional details expected to be released following the staff town hall. The restructuring reflects a broader industry-wide trend among legacy media companies across Australia and globally, as organizations grapple with declining print advertising revenue and shifting audience consumption habits that favor digital and mobile news content.

-

Merger deal between Paramount and Warner Bros paused by judge

In a major antitrust development shaking the global media industry, a United States federal judge has issued a temporary restraining order halting the planned $110 billion merger between entertainment heavyweights Paramount Skydance and Warner Bros. Discovery, blocking the combination for 14 days. The ruling comes in response to a high-stakes lawsuit filed by a coalition of 12 US states, led by California and New York, which argues that the proposed merger would cripple market competition and force higher costs for consumers across the country. Prosecutors representing the state coalition warned that merging two of Hollywood’s most prominent studios would inflict widespread harm on multiple stakeholders, from independent movie theater operators and basic cable distribution networks to the general audiences that consume their content. Lawyers for the two media conglomerates have pushed back against the claims, countering that state regulators have misjudged the current media landscape, and that merging their operations would unlock greater efficiency for their streaming platforms, which have faced mounting pressure in a crowded, highly competitive market. US District Judge Araceli Martínez-Olguín issued the 14-day injunction on Monday, one week after hearing oral legal arguments from both sides in the case. The court order explicitly prohibits either company from completing the merger or beginning any process of integrating their business operations during the two-week period. In her written ruling, Judge Martínez-Olguín emphasized that the coalition of states had raised substantial, credible questions about how the proposed merger would disrupt the existing ecosystem for motion picture distribution. She noted that if the court allowed the merger to move forward before reaching a final verdict, undoing the combination later would be functionally near-impossible, comparing it to the difficulty of “unscrambling the egg” once an egg has been broken and mixed. The judge also rejected the media companies’ core arguments, stating that the public’s critical interest in enforcing antitrust regulations to preserve competitive markets outweighs any disruption caused by a temporary pause to the merger process. She added that both Paramount Skydance and Warner Bros. Discovery remain fully operational, independent companies that can compete effectively in the open market while the legal process plays out. If the merger were to ultimately receive final approval, it would bring to an end a century of fierce head-to-head rivalry between two of Hollywood’s most iconic and successful entertainment creators. The combined company would control an unparalleled catalog of legendary entertainment franchises, ranging from *Harry Potter*, Batman, *Mission: Impossible* and *Top Gun* to major cable news and entertainment networks including CNN, MTV, and Nickelodeon. Industry analysts estimate that a merged Paramount-Warner Bros. entity would be responsible for more than a quarter of all major theatrical film releases in the United States, giving it unprecedented leverage over distribution and pricing across the sector. Monday’s ruling marks a significant early setback for the two companies, which have been pushing for the merger as a strategy to better navigate the ongoing upheaval and intense competition that defines the modern streaming landscape. The next court hearing to evaluate the case has been scheduled for August, where both sides will present further arguments ahead of a final ruling on whether the merger can proceed.

-

AliExpress fined record €550m by EU for allowing sale of illegal goods

In a landmark enforcement of the European Union’s landmark Digital Services Act (DSA), Chinese e-commerce giant AliExpress has been issued a record €550 million penalty for systemic failures to stop the sale of counterfeit and unsafe products across its platform to millions of European consumers. The penalty, the largest ever handed down under the DSA, follows a two-year investigation that uncovered widespread gaps in AliExpress’s risk assessment and product compliance systems, regulators announced Wednesday.

AliExpress, a subsidiary of Chinese tech conglomerate Alibaba, boasts 193 million monthly active users across the European Union — a larger user base than competing Chinese fast-fashion platforms Shein and Temu, according to EU data. The investigation concluded that the platform’s automated detection tools for illegal products failed to flag thousands of dangerous and counterfeit listings, while flagged items often remained active on the site for weeks before being removed. Regulators also found that AliExpress did not enforce meaningful penalties against third-party sellers offering illegal goods, and that basic compliance checks could be easily bypassed by bad actors.

EU Digital Commissioner Henna Virkkunen emphasized that the circulation of harmful counterfeit goods is not an inevitable downside of e-commerce, but a direct result of AliExpress’s failure to meet its legal obligations under EU law. “The spread of counterfeit clothing, unsafe toys, dangerous cosmetics and other illegal and harmful products is not an unavoidable cost of shopping online — it is a failure by AliExpress to comply with its obligations,” Virkkunen said in a statement.

The DSA, which went into full effect for large online platforms last year, requires major tech providers to implement rigorous due diligence to remove illegal and harmful content from their services, with maximum fines reaching 6% of a company’s global annual turnover. Alibaba reported €122 billion in global turnover last year, meaning the maximum possible fine could have exceeded €7 billion, making the €550 million penalty far lower than the allowed cap.

AliExpress has pushed back against the ruling, calling the fine disproportionate and arguing that it does not reflect the proactive upgrades the company has already made to its compliance systems. “We disagree with today’s decision and the disproportionate fine, which does not adequately reflect our established framework and the significant, proactive enhancements we have made,” a company spokesperson said. The platform added that it is currently reviewing the commission’s ruling and evaluating all legal options to challenge the penalty. AliExpress is required to pay the fine and submit a corrective action plan addressing the identified breaches to the European Commission by October 20.

This penalty marks the latest in a series of high-profile enforcement actions against large online platforms under the DSA. Earlier this year, competitor Temu was fined €200 million for failing to curb sales of unsafe children’s products, and last year Elon Musk’s social media platform X was hit with a €120 million fine over deceptive verification practices that exposed users to widespread scams.

-

EU hits AliExpress with a record 550 million-euro fine over unsafe and counterfeit goods

BRUSSELS – In a landmark enforcement of the European Union’s landmark Digital Services Act (DSA), the European Commission announced Monday that it has issued a €550 million ($629 million) fine to Chinese e-commerce giant AliExpress, marking the largest penalty ever handed down for violations of the bloc’s sweeping digital regulation. The penalty comes on the heels of similar enforcement actions against other major platforms, setting a clear precedent for the EU’s aggressive crackdown on non-compliance by global online marketplaces operating in its single market.

This latest fine follows a €200 million penalty issued to another China-based online retailer, Temu, just months prior, and a $120 million penalty imposed last year on X, the social media platform owned by Elon Musk, for failing to meet DSA obligations. For AliExpress, the penalty also arrives less than three weeks after its parent company, Chinese tech conglomerate Alibaba, agreed to pay $600 million to settle a long-running dispute with U.S. authorities over claims the firm facilitated the import and sale of illegal pharmaceuticals, controlled substances, regulated chemicals and pill-manufacturing equipment into the United States.

European officials emphasized that the fine stems from AliExpress’s persistent failure to systematically curb the trade of dangerous and illicit goods on its platform, including counterfeit apparel, children’s toys that fail EU safety standards, toxic cosmetics, and a range of other prohibited products that put consumers at risk. Henna Virkkunen, the European Commission’s Executive Vice-President responsible for tech sovereignty, security and democracy, stated in an official release that the proliferation of these harmful goods is not an inevitable side effect of online commerce, but a direct result of AliExpress falling short of its mandatory obligations under the DSA.

“Scale is not an excuse; risks must be identified and addressed systematically to ensure consumers can safely shop online,” Virkkunen said. “Today, we are holding AliExpress to this standard and request it to take urgent corrective action.”

The commission’s investigation found that up until the bloc’s preliminary ruling in June 2024, AliExpress had not implemented sufficient safeguards to root out illegal and unsafe listings across its platform. While the company offered formal commitments to upgrade its compliance systems following the preliminary finding, the commission still moved forward with the full penalty to reflect the severity of the earlier non-compliance. AliExpress now faces an October 20 deadline to submit a detailed, actionable remediation plan outlining concrete steps it will take to address gaps in its systemic risk assessment and mitigation processes.

Enshrined into EU law in 2022 and fully enforceable for major platforms since early 2024, the DSA is a landmark regulatory framework designed to protect digital users by forcing large online platforms to crack down on illegal and harmful content—ranging from dangerous counterfeit goods to incitement of violence and genocide—while upholding European citizens’ fundamental rights to privacy and free speech. The regulation requires very large online platforms, defined as those with more than 45 million monthly active users in the EU, to conduct regular mandatory risk assessments and implement targeted mitigation measures to address systemic harms tied to their services.

In a written response emailed to the Associated Press following the announcement, AliExpress pushed back against the penalty, arguing it has made substantial proactive investments to align its operations with DSA requirements since the regulation entered into force. The company said it “has been, and continues to be, firmly committed to meeting our obligations and we have invested substantial resources in risk assessment and mitigation, product safety and consumer protection.”

AliExpress rejected the fine as disproportionate, claiming it does not fairly reflect the compliance framework the company has already built, nor the significant upgrades it has already rolled out to strengthen safety protocols. “We are carefully reviewing the decision and considering all available options,” the company added, leaving the door open to an appeal of the penalty.

-

Mamamia appoints son of founder Mia Freedman as its new CEO

One of Australia’s biggest independent digital media companies, Mamamia, has ushered in a new era of leadership with the appointment of 28-year-old Luca Lavigne — the son of founder Mia Freedman — as its newest chief executive officer.

Founded by Freedman in her own living room back in 2007, Mamamia has grown from a small personal project into one of the nation’s most prominent independent media voices focused on women’s content. Lavigne’s rise to the top role is not a sudden handout: he has worked his way up through every tier of the company over the past decade, starting his tenure as an 18-year-old intern straight out of school. After cutting his teeth across multiple departments, he stepped into the chief operating officer role just two years ago, and has now been promoted to the top spot vacated by outgoing CEO Nat Harvey, who departed Mamamia to take up a new leadership position at Southern Cross Media Group.

The announcement of Lavigne’s appointment was made public during a recent episode of the Mumbrella podcast, where the new CEO opened up about his career trajectory, his connection to the company’s founding team, and his plans for the future. In a candid conversation, Lavigne first paid warm tribute to his predecessor, praising Harvey’s unmatched ability to inspire teams across the organization.

“CEO really stands for chief energy officer, and Nat is the best example of that,” Lavigne said. “I’ve never met anyone who can get up in front of a group of people and inspire them as Nat can, and I’m going to miss that about her hugely.”

Ahead of inevitable public and media scrutiny over his family ties to the company’s leadership — Freedman is his mother, and his father Jason Lavigne also serves as a company director — Lavigne was open about how he first joined the company, while pushing back against assumptions that his promotion was unearned. He acknowledged that his family connection gave him the initial foot in the door a decade ago, but emphasized that Mamamia’s culture does not allow leaders to rest on their family connections.

“Let’s be honest about how I got in the door here 10 years ago, the co-founders and I go back a long time. We’ve known each other a while, I’m not going to insult anyone’s intelligence by pretending otherwise,” he joked. “What I do know is that Mamamia is not a place that you can coast.”

Outgoing CEO Harvey also publicly defended Lavigne’s appointment, noting that his decade of hands-on experience, relentless work ethic, and proven contributions to the business leave no question about his suitability for the role. “There will be nobody in this business, certainly over the last 12 months, that would question Luca’s work ethic or contribution or ability to do the job,” she said.

Reflecting on his rapid career progression, Lavigne noted that taking on senior roles earlier than the industry average has become a pattern for him: after starting at 18, he is now taking on the CEO role at 28, and just recently welcomed newborn twins, bringing his total number of children to three. “I found my first grey hair the other day, which I think says a lot about where I’m at in my life,” he joked. “I’ve also just had newborn twins, I’ve got three kids at home. So it seems to be a pattern in my life that I seem to do things a little early.”

-

Ryanair profits drop as Iran war puts off passengers and lifts fuel costs

Europe’s largest low-cost carrier Ryanair has reported a sharp 34% year-on-year drop in pre-tax profits for the first quarter of its financial year (April to June), as the resurgent conflict in the Middle East sends jet fuel costs soaring and sparks widespread consumer hesitation to book air travel in advance. The Irish airline posted pre-tax profits of €593 million (£503 million) for the three-month period, with overall revenue seeing almost no growth, edging up just 1% to €4.4 billion, as the carrier was forced to slash ticket prices to stimulate flagging demand amid geopolitical uncertainty.

-

Scott Pape has compared switching super strategies to a married man on Tinder

Well-known Australian finance commentator Scott Pape, popularly known as the Barefoot Investor, has issued a sharp warning to Australian superannuation holders against making impulsive portfolio changes in response to viral market crash warnings, using a striking analogy to drive his point home. Pape’s comments came after a 42-year-old superannuation member, identified only as James, reached out for guidance following a high-profile podcast appearance from veteran investor Jeremy Grantham.

Grantham, the British billionaire co-founder of global asset management firm GMO who built his reputation for correctly predicting both the 2000 dot-com collapse and the 2008 global financial crisis, recently appeared on *The Diary of a CEO* podcast. In that episode, titled “Billionaire’s WARNING: I’m SELLING. The Crash Is Already Here!”, Grantham doubled down on his long-held claim that the U.S. stock market is currently the largest investment bubble in American history. He predicted a catastrophic 70% downturn, dismissed cryptocurrency as worthless, and drew parallels between the ongoing artificial intelligence boom and the unsustainable dot-com bubble of the late 1990s.

Alarmed by Grantham’s warnings, James told Pape he planned to reallocate his superannuation and personal investment holdings away from U.S. and Australian equities over fears of an imminent market collapse. Pape responded by acknowledging that he does not fault James for feeling anxious, but made clear he found the podcast itself reckless. Pape compared the clickbait-driven warning to a married man mindlessly swiping through dating app Tinder: a provocative act designed to spark unnecessary dissatisfaction with a stable, long-term arrangement in favor of a riskier, more glamorous alternative.

“That podcast felt like the financial version of a married bloke on Tinder,” Pape wrote in his latest advisory post. “The whole thing is designed to make you restless and think ‘Maybe I should ditch my boring old index funds for some sexy emerging markets.’” He went on to dismiss the strategy of timing the market based on crash predictions as a “rubbish way to invest your money.”

Notably, Pape conceded that he actually agrees with much of Grantham’s core analysis: U.S. and Australian equities do show signs of significant overvaluation right now. Where he disagrees sharply is with the advice for ordinary retail investors to sell their holdings and exit the market in anticipation of a crash. Pape pointed out that profiting from a market crash requires being correct not once, but twice: an investor must sell before the downturn hits, then correctly time their re-entry to buy back in at the bottom. That kind of consistent market timing is notoriously difficult even for professional investors, he argued.

As evidence, Pape noted that Grantham has been labeling the U.S. stock market a bubble since 2021. In the years since his first warning, the S&P 500 has still surged more than 100%, leaving investors who followed his early advice out of the market and missing out on massive gains.

For ordinary long-term investors like James, who is 42 and has decades of contributing to and growing his superannuation before retirement, Pape advocated for a “married to your portfolio” approach. He explained that he committed to his own diversified holdings years ago, vowing to stick with them through both market booms and corrections. Historical data, he noted, consistently shows that equities deliver stronger long-term returns than any other major asset class, even with periodic steep crashes.

“Every crash has eventually been followed by new highs,” Pape said. “So I keep a few months’ cash in the bank and accept that happily ever after only exists in fairy tales.” His advice to James and other anxious Australian superannuation holders is straightforward: stay committed to a diversified long-term equity portfolio, keep a cash buffer to avoid being forced to sell during a downturn, and avoid the hype-driven “spicy dating apps” of viral market crash predictions.