Global equity markets delivered a mixed performance on Friday, with U.S. futures sliding downward as fading optimism over a recent U.S.-Iran war-ending ceasefire offset early market gains. The uptick in geopolitical risk came after high-stakes negotiations over Iran’s nuclear program and the full reopening of critical oil shipping lanes through the Strait of Hormuz were postponed at the last minute.

U.S. stock exchanges were closed Friday in observance of the Juneteenth federal holiday, leaving futures as the main indicator of market sentiment heading into next week’s trading session. Alongside the delayed Iran talks, fresh conflict erupted in the Middle East overnight: Israel’s military confirmed it carried out strikes across multiple targets in southern Lebanon, while the Lebanese militant group Hezbollah reported heavy combat in the same region, stoking broader fears of regional escalation.

While both Washington and Tehran have signaled willingness to negotiate a lasting peace settlement, analysts warn the current tentative agreement remains vulnerable on multiple fronts. “Both sides are trying to project good faith to markets,” noted Bas van Geffen, senior macro analyst at RaboResearch, in a market commentary Friday. “But even if surface tensions appear to have eased, powerful underlying risks remain. The ceasefire agreement remains fragile across multiple fronts.”

European equities closed the session with modest mixed moves. Germany’s benchmark DAX index gained 0.2% to end at 25,079.30, while France’s CAC 40 held nearly steady at 8,467.75, edging just a fraction of a percent lower. The UK’s FTSE 100 slipped 0.2% to close at 10,376.64. Across the Atlantic, S&P 500 and Dow Jones Industrial Average futures both fell 0.2% in early Friday trading, pointing to potential downward pressure when U.S. markets reopen next week.

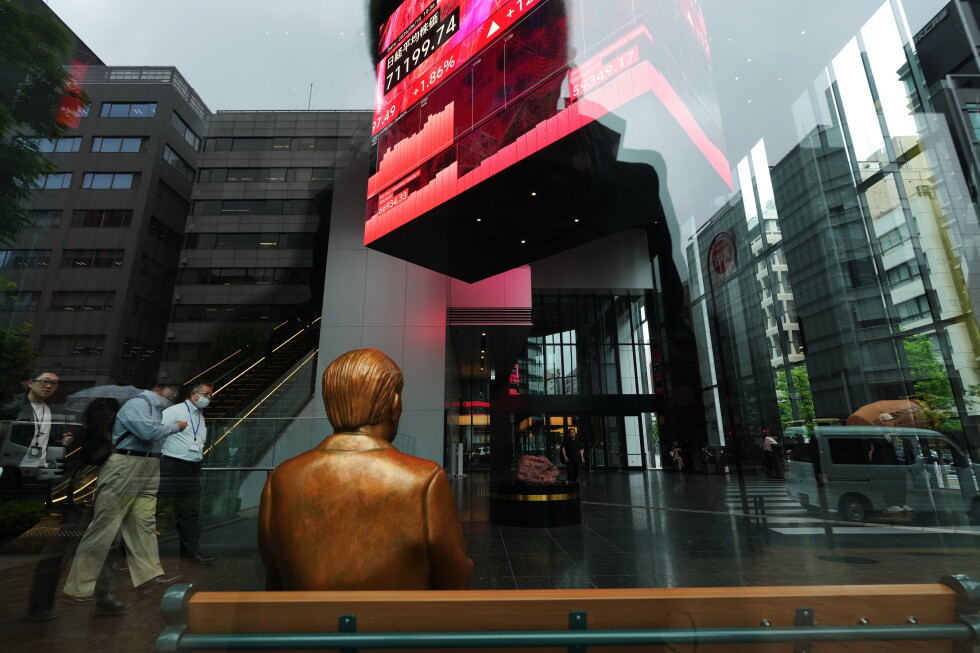

In Asian markets, Japan’s Nikkei 225 swung between small gains and losses through the session before closing 0.3% higher at a fresh all-time record of 71,250.06. The benchmark close came days after the Bank of Japan made a historic policy shift, raising its benchmark interest rate to 1% — a 30-year high — after years of near-zero and negative rate policies meant to stimulate stagnant growth. The move was driven by mounting inflation pressures, which government data released Friday showed remained steady in the latest reading: core consumer prices, which exclude volatile fresh food costs, held steady from the previous month. Analysts forecast core inflation will likely tick upward in coming months even amid elevated global fuel costs.

Other major Asian indexes ticked downward to close out the week. South Korea’s Kospi shed 0.1% to end at 9,052.42, just below the record high it set in the previous session. Australia’s S&P/ASX 200 fell 0.9% to 8,828.70, while India’s Sensex dropped 0.8% from its previous close. Markets across greater China — including Hong Kong, Shanghai and Taiwan — were closed Friday for the Dragon Boat Festival public holiday.

The mixed Friday performance followed a strong rally on Wall Street Thursday, where major indexes erased most of the prior session’s losses to lock in weekly gains. The rally was led by blockbuster gains for large-cap technology stocks, which lifted the S&P 500 1.1% higher, the Nasdaq composite 1.9% higher, and the Dow Jones Industrial Average 0.1% higher. The Wednesday sell-off that preceded the rally had been driven by growing investor expectations that the U.S. Federal Reserve will raise interest rates before the end of 2025 to cool persistent inflation. The Fed held rates steady at its most recent policy meeting this week, but official commentary left the door open for a coming hike.

Semiconductor stocks led Thursday’s rally, after former U.S. President Donald Trump announced that Intel would manufacture cutting-edge chips for Apple entirely within U.S. facilities. Intel surged 10.6% on the news, pulling other major semiconductor players higher: Nvidia gained 3% and Micron Technology jumped 8.7%. One notable laggard was SpaceX, which fell for the second consecutive session following its highly anticipated public market debut last week. The Elon Musk-led aerospace and artificial intelligence firm dropped 3.6% Thursday after falling 4.9% in the previous session.

Energy markets also saw volatile trading this week, following the U.S.-Iran ceasefire agreement that reopened the Strait of Hormuz — the chokepoint through which roughly 20% of global oil shipments pass. Brent crude, the global benchmark, ended Thursday trading up 0.4% at $79.85 per barrel after spending most of the session in negative territory. U.S. benchmark West Texas Intermediate crude fell 0.2% to $75.85 per barrel. Early Friday, Brent was down 0.4% at $79.50 per barrel, while U.S. crude held steady at $75.85.

While oil prices remain well above the roughly $70 per barrel level seen before the U.S.-Iran conflict erupted, they are still far below the triple-digit prices recorded just a few weeks ago. Elevated energy costs have added significant pressure to already high global inflation, with U.S. gasoline prices dipping just below $4 per gallon in recent weeks but still holding 25% higher than year-ago levels. Broad-based cost pressures across shipping and energy have pushed prices higher for a wide range of consumer and industrial goods.

In currency markets, the U.S. dollar edged slightly lower against the Japanese yen early Friday, falling to 161.31 yen from 161.38 yen in the previous session. The euro held steady at $1.1458 against the greenback to close out the week.