The global automotive sector is undergoing a seismic shift, as long-dominant American, European, and Japanese car manufacturers rapidly lose market share to ambitious Chinese rivals that are leading the industry not just in electric vehicle (EV) production, but across batteries, intelligent design, and automotive software.

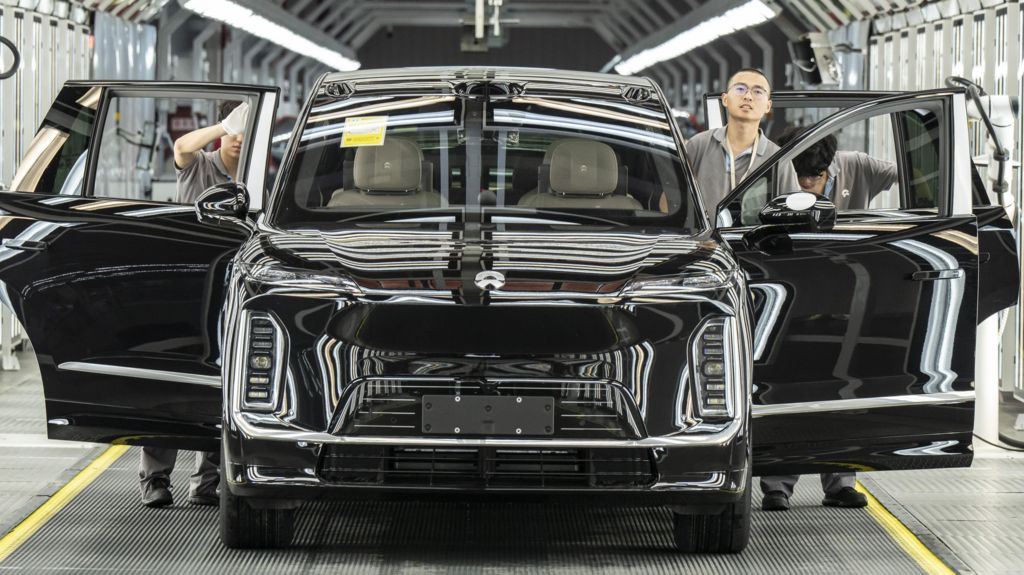

During on-the-ground reporting at Chinese manufacturing facilities in Beijing and Hefei, conducted alongside 2026’s Auto China — the world’s largest automotive exhibition — the BBC observed industry-leading levels of production automation and unprecedented speed in software development. These capabilities have left once-dominant foreign brands scrambling to catch up in the world’s largest single car market.

Following a tour of a highly automated Shanghai EV factory, Honda CEO Toshihiro Mibe told Japanese media bluntly: “We have no chance against this.” Ford CEO Jim Farley has similarly issued a stark warning, noting that Western automakers are “in a fight for our lives” as Chinese brands expand their footprint across global markets.

After decades of structuring their Chinese operations around joint ventures with local partners to access the massive domestic market, global carmakers are fundamentally restructuring these partnerships to remain competitive in the new EV era.

Shanghai-based automotive analyst Bill Russo argues that the developed world has fundamentally misunderstood this industry transition. “The biggest mistake that the developed world is making is believing that the transition is only about electric cars,” he explained. “It’s about who will lead the next generation of mobility technology.”

China’s competitive advantage extends far beyond finished passenger vehicles. Data from the Rhodium Group shows that China is now the top exporter for over 315 product categories, up from just 163 in 2016. A large share of these categories are core components of the EV supply chain, including lithium-ion batteries, critical manufacturing equipment, and specialized vehicle parts.

Analysis from the International Energy Agency confirms that producing a small electric SUV in China costs at least 30% less than manufacturing the same vehicle in advanced Western economies, a gap driven largely by lower battery production costs and China’s highly integrated, efficient domestic supply chain network.

This massive competitive advantage was built over decades of targeted policy support. Rhodium Group estimates that China has directed tens of billions of dollars in public support to EV and battery manufacturing in just the past few years alone. These subsidies, which have faced fierce criticism from policymakers in the European Union and United States for distorting global markets, have allowed Chinese firms to scale production rapidly and bring down consumer prices.

Intense competition within China’s domestic market has also accelerated the pace of innovation. Major Chinese technology giants including Xiaomi, Huawei, and Alibaba have all entered the EV space in recent years, bringing deep expertise in consumer technology and software integration to the automotive sector. Russo notes that Chinese manufacturers are no longer focused on catching up to Western rivals — instead, they are competing directly with each other, driving constant improvement. “They’re not racing the West anymore, they’re racing each other,” he said.

As modern vehicles become increasingly software-defined, from advanced driver assistance systems to in-vehicle entertainment and connectivity, these technology firms have given Chinese automakers a critical edge. The pace of progress is on clear display at Xiaomi’s EV factory outside Beijing, where a fully completed vehicle rolls off the production line approximately every 76 seconds. Though Xiaomi only launched its first electric vehicle in 2024, it has already climbed to become one of China’s top 10 best-selling EV brands. Its signature strategy integrates vehicles with smartphones, mobile apps, and smart home ecosystems to create a seamless connected user experience.

At Nio’s production facility in Hefei, large sections of the assembly line operate almost entirely without human intervention. Industry leader BYD has developed an ultra-fast charging technology that can add 400 kilometers (249 miles) of driving range in roughly five minutes, bringing EV charge times close to the length of a traditional gasoline refueling stop.

XPeng founder and CEO He Xiaopeng told the BBC that his company is now prioritizing research and development into humanoid robots and flying cars alongside its core EV business. “In the next decade, any car company will also be a robotics company,” he predicted.

Global automakers already depend on China as a manufacturing and export hub for international markets: Tesla exports Shanghai-assembled Model 3 sedans to customers across Europe, while BMW produces electric Mini models in China for global distribution. Despite this, most foreign brands have struggled to maintain their position within China’s own domestic market.

Data from automotive consultancy Automobility shows that foreign brands’ combined share of China’s domestic car market has plummeted from 64% in 2020 to just 32% in 2026. This steep decline has hit bottom lines at General Motors and major German manufacturers, which once relied heavily on China for a large share of their global profits. Even luxury automotive brands are facing growing pressure: Huawei’s Maextro S800 luxury sedan is now the best-selling vehicle priced above $100,000 (£74,145) in China, outselling the combined total of one-time market leaders including the Porsche Panamera and BMW 7-series.

Today, China exports roughly seven million finished vehicles annually, with nearly half of those shipments being electric vehicles. For decades, the dynamic between foreign and Chinese automotive firms followed a clear pattern: global brands brought advanced technology and established brand recognition, while local partners provided manufacturing infrastructure and access to the Chinese market. That model is now obsolete, and industry relationships are being redefined from the ground up.

Stellantis recently finalized a €1 billion ($1.16 billion; £863 million) agreement with state-backed Chinese automaker Dongfeng to produce Peugeot and Jeep models in China for both domestic and global sales. As part of the deal, Stellantis will also bring Dongfeng’s Voyah electric brand to the European market, and is currently exploring the possibility of producing Chinese-designed vehicles at its existing manufacturing plant in France.

Volkswagen has invested $700 million to access XPeng’s software architecture and autonomous driving systems to accelerate development of its next-generation EV line — a move that marked an implicit acknowledgment that the German giant could not develop the technology quickly enough on its own in its home markets. XPeng’s He framed the partnership as mutually beneficial: “We study each other, so we trust each other, so we help each other.”

Toyota, Hyundai, Ford, and Nissan have all followed similar paths, expanding their Chinese research and development centers or exploring plans to build Chinese-designed vehicles at their overseas factories, tapping into local Chinese innovation and engineering talent rather than just using the country for low-cost assembly.

Not all global automakers have successfully adapted to the new landscape. Audi has been forced to offer steep discounts on its E5 model, a vehicle specifically designed and engineered for the Chinese market, after demand fell far short of company projections. General Motors has written down billions of dollars in value from its Chinese operations, and reported a more than 21% drop in sales in China during the first quarter of 2026.

Japanese automakers have been particularly slow to transition to fully electric vehicles, leaving them exposed to competition in China and increasingly in Southeast Asia, where Chinese brands are rapidly capturing market share. In early 2026, Volkswagen briefly reclaimed the title of top-selling car brand in China, but industry analysts attribute the shift largely to the phase-out of Beijing’s EV subsidies, which temporarily weakened domestic Chinese rivals.

China’s domestic automotive market is also cooling after years of breakneck expansion. Industry growth has slowed, while persistent overcapacity and an intense industry-wide price war are squeezing profit margins for nearly all players. This market pressure is a key driver of Chinese automakers’ push into overseas markets: major brands including BYD, Chery, and SAIC are aggressively expanding into Europe and emerging markets across the Global South, even facing EU tariffs as high as 45% on Chinese EV imports.

Chery’s Jaecoo 7 has already become one of the United Kingdom’s best-selling new passenger models within just 14 months of its launch. However, tariffs of more than 100% have effectively blocked Chinese EV brands from accessing the large US market for the foreseeable future.

Industry analysts warn that as more vehicle production, battery innovation, and automotive software development shifts to China, established manufacturing hubs in Southeast Asia and Europe could face sustained disruption, putting local jobs and regional economic growth at risk. Trade tariffs will not be enough to shield domestic industries from this shift, says independent automotive consultant James Pearson: “If you lock them out of one market, they will just find another.”

Russo argues that the global automotive industry’s center of gravity has already shifted irreversibly toward China. Companies that are willing to collaborate and adapt to the new landscape have a chance to remain competitive, he says, while those that focus solely on blocking China’s rise will almost certainly fall further behind.