For nearly a century, diamond mining has been the beating economic heart of Sierra Leone’s Kono region, a land whose gem wealth once fueled a devastating decade-long civil war that left tens of thousands dead and indelible scars on local communities. Today, a far quieter crisis is reshaping life here: the global boom of lab-grown diamonds has sent natural diamond prices plummeting, forcing major mines to close and pushing thousands of out-of-work miners into scattered, unregulated small-scale digging operations where finds are increasingly rare.

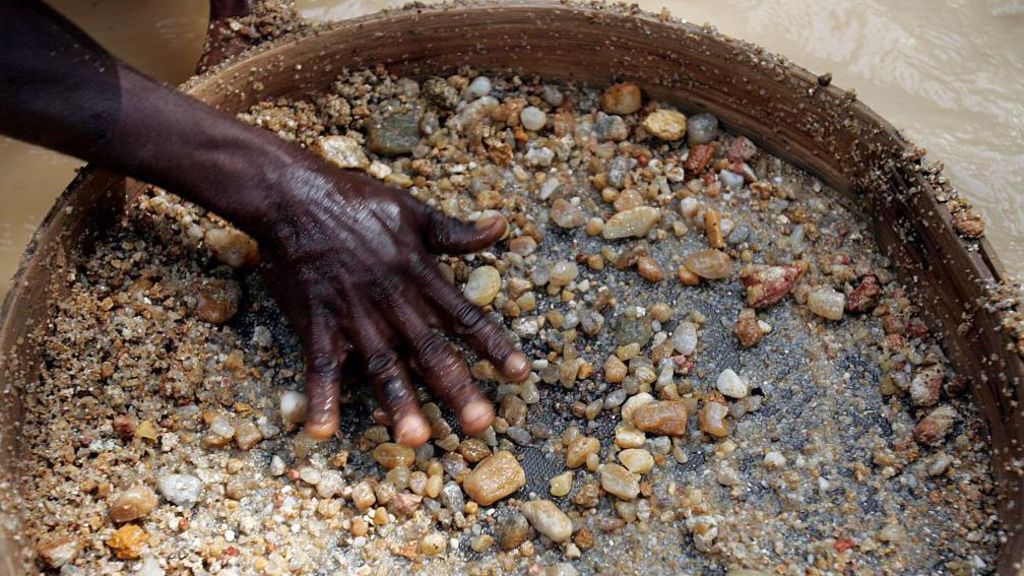

Under the unforgiving West African sun, Daniel, a foreman at one of these informal artisanal mines in Kono, works shirtless, sifting and shoveling wet mud by hand to hunt for tiny gem fragments. He and his five crew members know all too well how slim their odds are: even after days, weeks, or entire months of backbreaking labor, they often leave empty-handed. “I have not made a lot of money yet,” Daniel explained, running his fingers through a pile of sorted gravel. “Sometimes for the whole of the year you can’t get anything. It is by the grace of God that you find a diamond. We are just dreaming, really. We still have that hope.”

His uncertain daily reality has become far more common since the 2024 closure of Koidu Holdings, Sierra Leone’s largest commercial diamond mine, which cut 1,000 jobs amid a bitter wage dispute. While the company officially cited dispute-related costs and security concerns for the shutdown, industry insiders privately acknowledge that slumping global natural diamond prices were a major contributing factor. Over just four years, retail prices for polished mined diamonds have fallen by roughly 40%, with the rapid expansion of the lab-grown diamond industry widely identified as the core driver.

Chemically and physically identical to mined diamonds, lab-grown diamonds are produced from crystallized carbon, mostly in manufacturing facilities in India and China, using either high pressure high temperature (HPHT) or chemical vapour deposition (CVD) technologies. They sell for up to 70% less than natural mined gems, a price point that has resonated deeply with cost-conscious consumers. Kono Governor Augustine Shekho confirmed the severe impact of the price collapse on the local economy: “Lower diamond values have reduced earnings for miners, constrained investment, and weakened local economic activity.”

The region’s complicated relationship with diamonds dates back decades. Kono’s gem reserves made it a key battleground during Sierra Leone’s 11-year civil war that ended in 2002, leaving over 50,000 people dead and hundreds of thousands displaced or maimed. Shekho lost his own mother to the violence, when armed factions fought for control of diamond deposits and terrorized local communities. “They shot at random, they killed people, burnt the entire town,” he recalled. “It was a war of terror… It was a nightmare. I would really not want to think about it.”

In 2003, the UN-backed Kimberley Process certification scheme was launched to block conflict “blood diamonds” from entering global markets, but the industry has never fully shaken its damaged reputation. Even today, many local residents question whether the region’s diamond wealth has ever delivered widespread prosperity. “To me the diamonds have failed us,” said Abubakar Amara, a primary school teacher in Kono. “What have those diamonds done for our community, for Kono, for Sierra Leone? We are considered as poor in the world.”

Industry giant De Beers, the British multinational that dominates global diamond marketing and mining, is attempting to reverse natural diamonds’ declining fortunes with a new initiative called Gemfair, a fair-trade style program for Sierra Leone’s artisanal miners. The project provides small-scale diggers with upgraded equipment, professional training, and access to more transparent pricing and direct market connections. “The idea is to connect with markets so that they can be able to find a place to sell their diamonds, and also to empower them, give them training, we give them skills,” explained Raymond Alpha, Gemfair’s local representative.

For De Beers, the initiative also serves a key reputational goal: it enables full traceability, letting retailers share the origin story of each mined diamond with consumers, who increasingly want to know the source of high-stakes purchases like engagement rings. “With people increasingly wanting to know where their coffee, cotton or chocolate has come from, it’s not surprising that people also want to know where their diamond – one of the most emotionally significant purchases – has come from,” said De Beers representative David Johnson.

But even with improved traceability and ethical branding, analysts do not expect lab-grown diamonds’ growth to slow. Rohit Mehta, chief executive of Forlink Ventures, a commodity firm based in Surat, India – the global hub of lab-grown diamond production – argues that lab-grown gems hold three key advantages over natural stones: lower cost, ethical production, and a smaller environmental footprint. “People are more conscious about climate change, about extracting too much from the earth,” he said.

That claim of environmental friendliness is disputed, however. Unlike mined diamonds, lab-grown production is extremely energy-intensive: creating a single carat of rough lab-grown diamond requires massive amounts of electricity, with production reactors running at temperatures comparable to the sun’s surface, according to Stanley Mathuram, a U.S.-based environmental consultant who studies the lab-grown diamond industry. “They’re like data centres. That’s the kind of energy that they require,” he noted.

Even so, energy concerns have done little to dampen consumer demand. One industry analysis projects the global lab-grown diamond market will grow from its 2024 valuation of $29.5 billion (£21.9 billion) to $91.9 billion by 2034. By 2025, the total market value of lab-grown diamonds already exceeds the $20 billion annual value of the global natural diamond jewelry market, per De Beers’ own estimates.

In the U.S., the 2026 Real Weddings Study from wedding platform The Knot found that lab-grown diamonds now make up 61% of all engagement ring sales, more than doubling their market share since 2022. The shift, the report notes, is driven by “economic pragmatism and evolving values,” with 40% of couples specifically prioritizing lab-grown stones for their rings. Atlanta-based jewelry retailer Doug Meadows, co-founder of David Douglas Diamonds, says consumers are primarily drawn to the chance to buy a larger stone for their budget. “It’s all about the stone. They’re going for the biggest bling that they can afford,” he explained. “Years ago, it used to be the diamond was the expensive part. With the advent of gold jumping up to $4,500, $5,000 an ounce, now the mounting is becoming a lot more expensive, and the diamond is becoming the cheap part.”

While Meadows sympathizes with efforts to promote natural diamonds, with their deep geographic and human origin stories, he acknowledges that convincing consumers to pay a premium is an uphill battle. “To try to educate a consumer about the value in a natural diamond, it is a new challenge,” he said. “I don’t know how we do it yet, I’m hoping the industry can give us an idea.”

Back in his small Kono mine, Daniel dumps another sieve of gravel into the mud, finding nothing. Head bowed, he stares at the pit before vowing to keep trying. “Unfortunately there is no diamond here,” he says. “I will try my luck again,” he adds, picking up his shovel to resume digging.