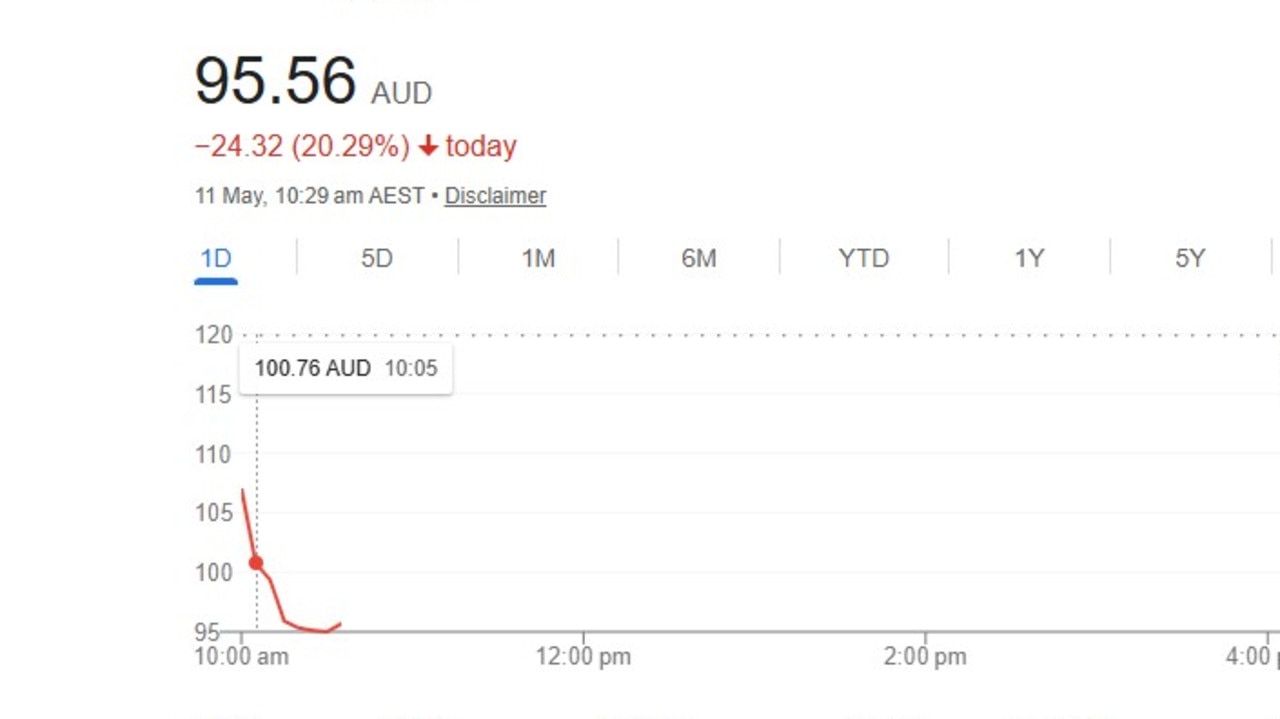

Australian healthcare multinational CSL has endured another severe market setback, with its share price plummeting 20.29% at market open to hit a 10-year low Monday, after the biotech giant disclosed a fresh $5 billion non-cash impairment write-down as part of a 90-day strategic review. The sharp drop pushed CSL’s share price below the $100 threshold for the first time since 2014, a dramatic fall from the company’s peak valuation of roughly $340 per share recorded at the height of the COVID-19 pandemic, when CSL saw explosive revenue growth driven by global vaccine rollouts.

Of the $5 billion total impairment, $1.5 billion was already accounted for in CSL’s first-half financial results, with the remaining charge reflecting underperformance across key international market segments. The company confirmed an additional $300 million write-down tied to its U.S.-based immunoglobulin business, while its albumin operations in China will take a $200 million hit from ongoing market headwinds. Weaker-than-projected revenue across these overseas segments weighed heavily on investor sentiment, leading to the historic single-day sell-off.

Despite the markdown, CSL reaffirmed its full-year financial projections, forecasting total annual revenue of roughly $21 billion Australian dollars and net profit of $3.1 billion Australian dollars, a modest downward revision from earlier estimates of $3.3 billion Australian dollars. The downgrade was announced by interim chief executive Gordon Naylor, who stepped into the top role just three months ago after former CEO Paul McKenzie’s abrupt departure earlier this year.

Naylor sought to reassure stakeholders Monday, noting that while the company’s long-term growth initiatives are progressing, their financial benefits will take longer to materialize than initial forecasts projected. As a result, CSL has revised downward its financial guidance through the 2026 fiscal year. The Monday announcement marks the second major market shock for CSL in just four months: back in August, the company lost $21 billion in market capitalization in a single trading session after unveiling a sweeping corporate restructuring plan. That restructuring includes cutting 3,000 global roles — an upfront cost of $770 million that is projected to generate annual savings of $500 million to $550 million over three years — as well as plans to spin off its influenza vaccine division Seqirus into an independent ASX-listed company by 2026. CSL will also merge the commercial and medical operations of its core blood plasma and iron deficiency treatment businesses into a single unified unit to streamline operations.

As a major exporter of plasma-derived life-saving therapies to the United States, CSL also addressed growing concerns over new U.S. tariffs on pharmaceutical products in its announcement. The company confirmed it does not expect any material impact from the tariffs, as the life-saving therapies it produces are set to be exempt from the new trade measures.